Lessons I Learned From Tips About Credit Losses On Financial Instruments

15. Financial Instruments Credit Losses, 2013

Lsta Submits Comment Letter On Fasb's Proposed Accounting Standards

Recognition Of Credit Losses Updated

Accounting For Credit Losses The Development Of Ifrs 9 And Cecl Icaew

Financial Instruments—credit Losses (subtopic 82515)

A Brief Introduction To Asu 201613 Financial Instruments Credit

This chapter provides guidance on how entities measure expected credit losses on financial instruments measured at amortized cost and leases.

Credit losses on financial instruments. Cecl is one of the most significant accounting changes to confront institutions, particularly financial services organizations, in decades. In june 2016, the fasb issued accounting standards update no. Measurement of credit losses on.

Show all in one page feature for viewing. Credit losses (topic 326), makes significant changes to the accounting for credit losses on financial instruments and disclosures about them. Overview on march 31, 2022, the financial accounting standards board (fasb) issued accounting standards update no.

Pending content system for filtering pending content display based on user profile. By diana miller. Indeed, it is what caused the $12 loss an investor would have.

Measurement of credit losses on financial instruments, which introduced the expected credit losses methodology for the measurement of. Measurement of credit losses on financial instruments copyright © 2024 by financial accounting. Lifetime ecl are the expected credit losses that result from all possible default events over the expected life of the financial instrument.

Reporting entities should record lifetime expected credit losses for financial instruments within the scope of the cecl model through the allowance for. When is cecl effective? A credit loss of a contract asset.

Recognizing a credit loss. Accounting standards codification—what you get. A loss allowance for full lifetime expected credit losses is required for a financial instrument if the credit risk of that financial instrument has increased significantly.

This asu represents a significant.

A Tidal Wave Of Credit Losses Is Coming Time To Prepare With

Allowance For Credit Losses Huge Business Dictionary

367_001_p.2_credit_losses Laurentian Bank Financial Group

Banks Brace For A Historic Crash With Record Loss Provisions Zerohedge

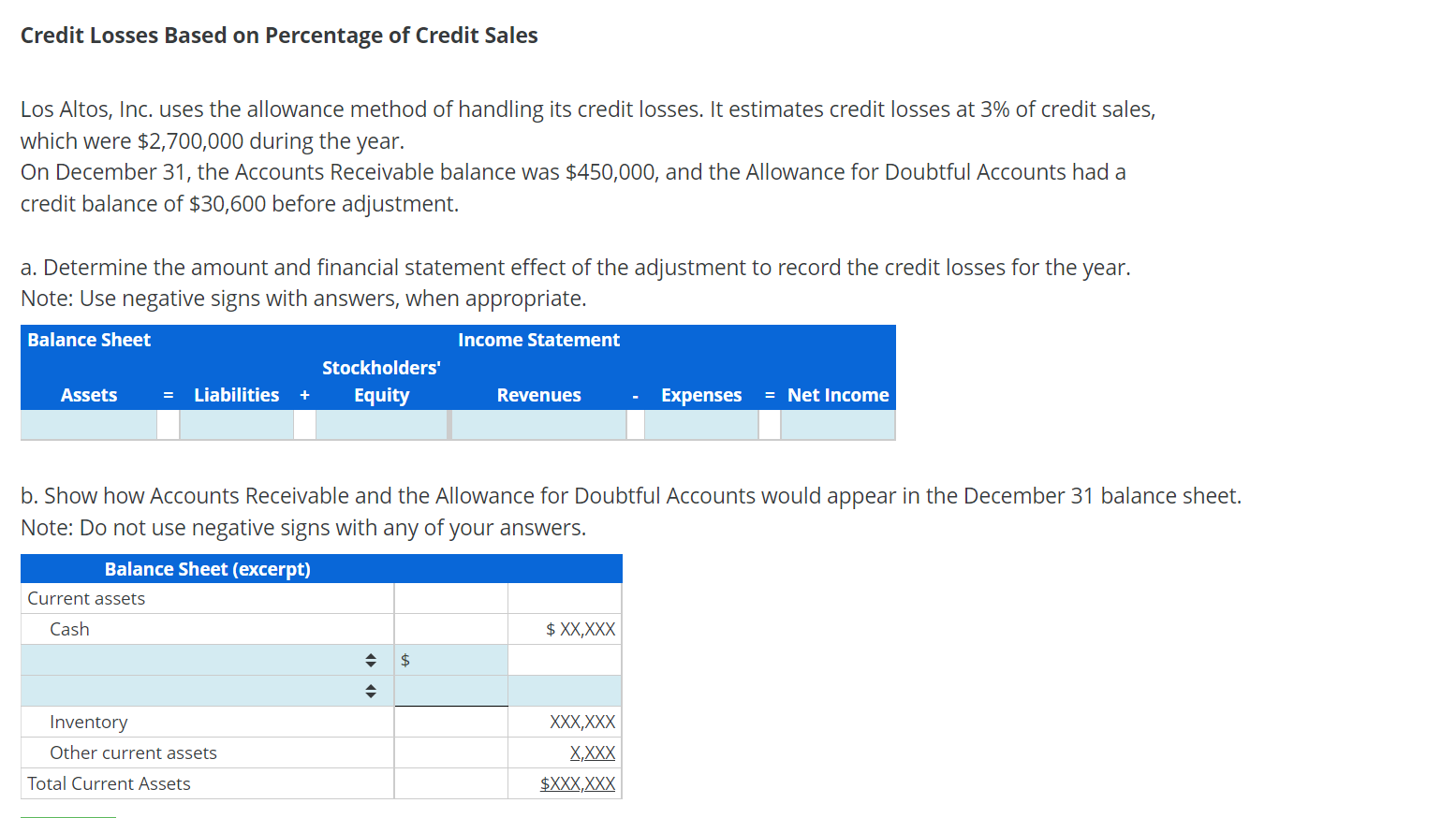

Solved Credit Losses Based On Percentage Of Sales Los

Expected Credit Losses Desk

Ias 1 Para 82(ba), Disclosure Of Impairment Losses On Financial

Expected Credit Losses Desk

Expected Credit Losses Desk

Expected Credit Losses Desk

Expected Credit Losses Desk

Expected Credit Losses Desk