The Secret Of Info About Consolidated Financial Statements After Acquisition

Consolidated Financial Statements Summary And Notes Huawei Annual

Fantastic Consolidated Statement Of Changes In Equity Bbs 1st Year

Consolidated Financial Statements India Dictionary

Consolidated Financial Statements Subsequent To Acquisition Date

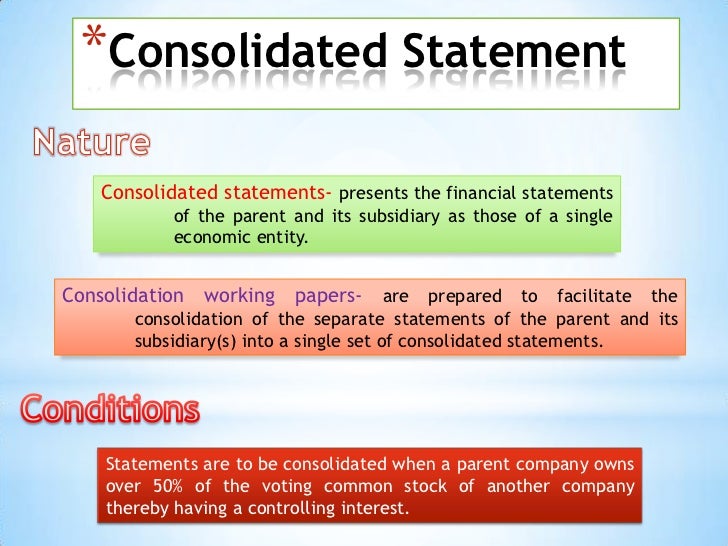

Consolidated Financial Statements Consolidation (business

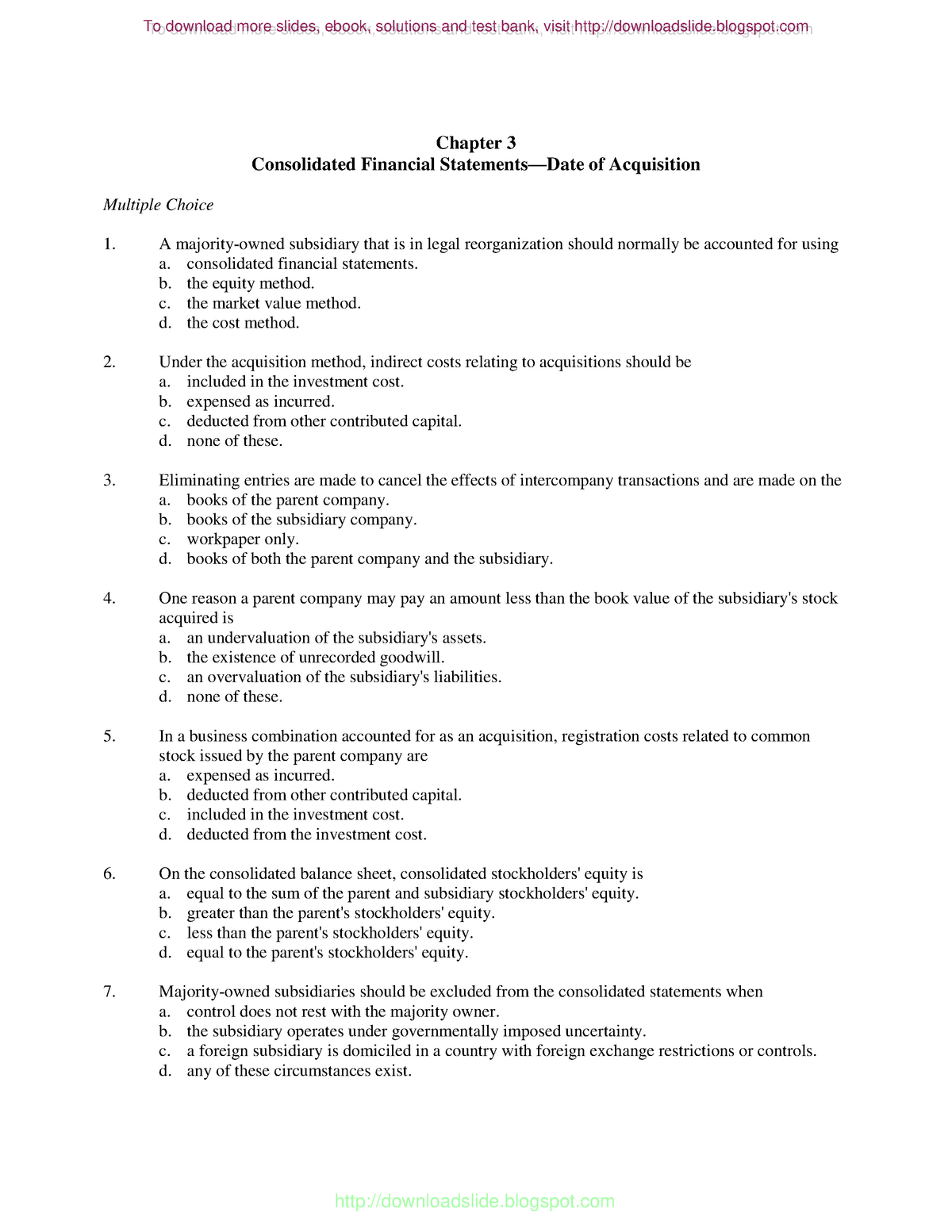

Quizzer Consolidated Financial Statements—date Of Acquisition

Consolidated financial statements are financial statements of an entity with multiple divisions or subsidiaries.

Consolidated financial statements after acquisition. The guidance in ifrs 10 consolidated financial statements is used to identify an acquirer in a business combination, i.e. The objective of consolidated financial statements is to present the results of the group in line with its economic substance, which is that of a single reporting entity. The partial equity method only partially accrues subsidiary income.

Ias 27 defines consolidated financial statements as ‘the financial statements of a group in which the assets, liabilities, equity, income, expenses and cash flows of the parent and its subsidiaries are presented as those of a single economic entity.’ the diagram below shows an example of a typical group structure: 2.9k views • 3 years ago. The significance tests are defined by the following fractions, expressed as percentages.

If an entity decides at a later point in time to acquire an additional portion of a subsidiary, the impact on the consolidated financial statement could be significant, because in accordance with ifrs 10 an acquisition of additional shares has to be treated as common control transaction. Compute total asset turnover and return on. The financial statements are generally in the name of the legal acquiree because the legal acquirer often adopts the name of the legal acquiree.

Recognize the complexities in preparing consolidated financial reports that emerge from the passage of time. [ifrs 3.7] [ifrs 3.7] if the guidance in ifrs 10 does not clearly indicate which of the combining entities is an acquirer, ifrs 3 provides additional guidance which is then. Control requires exposure or rights to variable returns and the ability to affect those returns through power over an investee.

Part 1 organizing your information download article 1 determine which holdings to report as subsidiaries. This article provides an introduction to ifrs® 3, business combinations and ifrs, 10 consolidated financial statements, including piecemeal acquisitions and disposals.

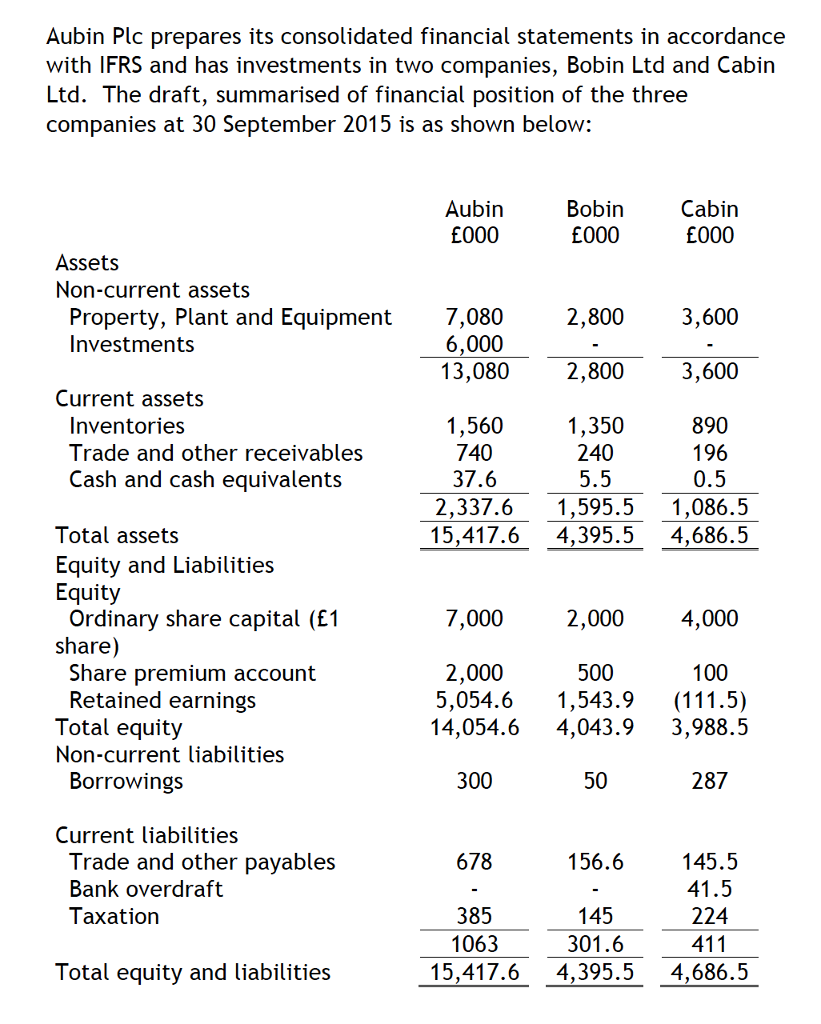

Determine consolidated totals subsequent to the date of acquisition. Consolidated financial statements are often referred to as ‘group accounts’. Upon completion of this chapter you will be able to:

The initial value method however, employs the cash basis for income recognition. As a result, a business combination has been formed from. The presentation of a consolidated group may require certain adjustments for transactions occurring between the reporting entity and its subsidiaries.

This playlist covers the difference between the cost method and equity method when preparing consolidated balance sheet and consolidated income statement. Ifrs 10 outlines the requirements for the preparation and presentation of consolidated financial statements, requiring entities to consolidate entities it controls. Ifrs 10 was issued in may 2011 and applies to annual.

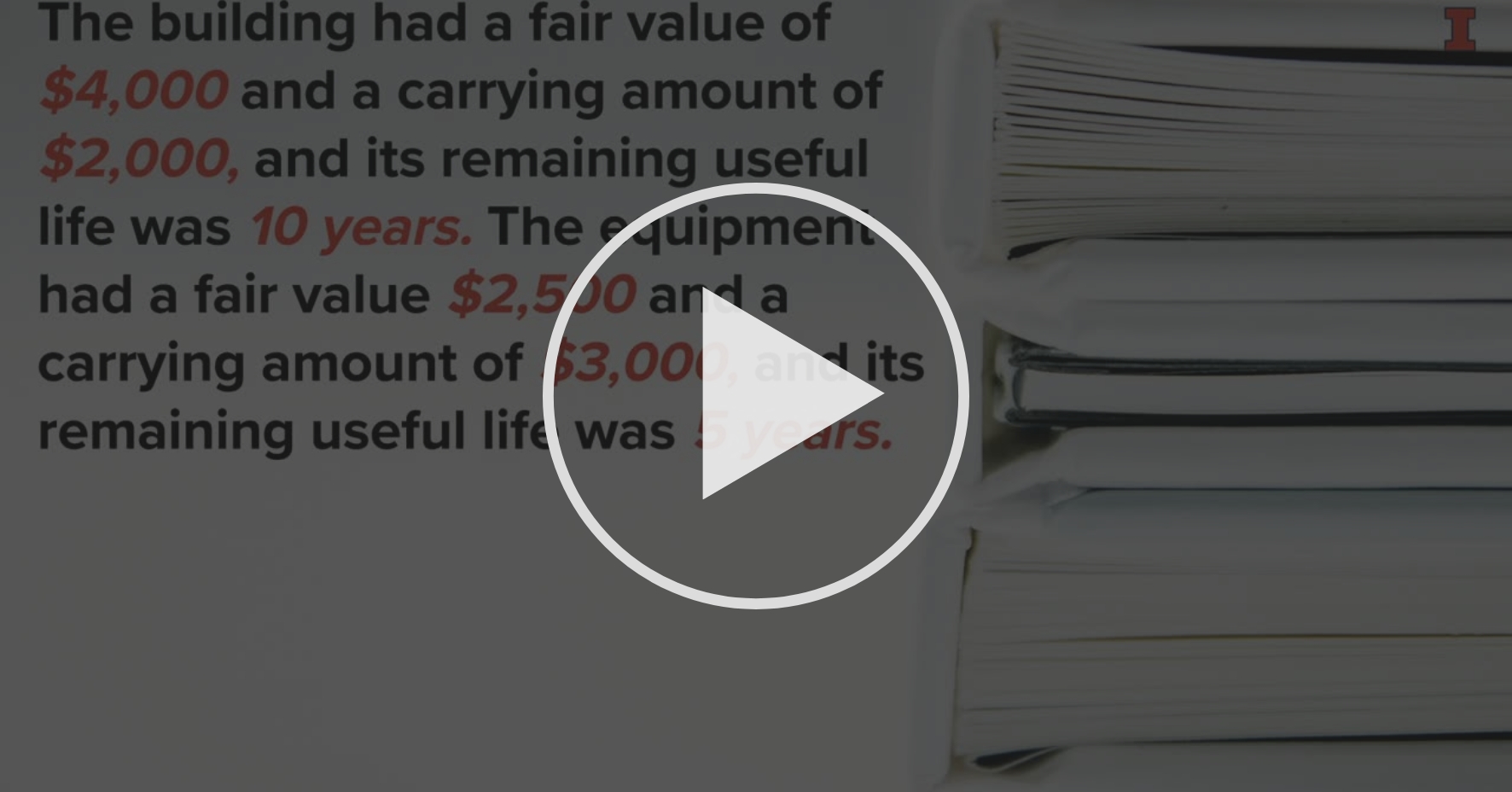

Explain the reporting of a subsidiary’s assets and liabilities when consolidated financial statements are prepared at the date of acquisition. Identify and describe the various methods available to a parent company in order to maintain its investment in subsidiary account in its internal records. Because only the retained shares (60 percent in this case) are consolidated, the parent must separately recognize any current year income accruing to it from its terminated interest.

Consolidated financial statements can be created easily using the following steps. Ifrs 10 outlines the requirements for the preparation and presentation of consolidated financial statements, requiring entities to consolidate entities it controls. Gaap, control is gained by the acquisition of over 50 percent of the voting stock of a company.

Consolidated Financial Statements Summary And Notes Huawei Annual

Consolidated Financial Statements Example.

:max_bytes(150000):strip_icc()/Consolidatedfinancialstatement_final-1a46c53d5f0d4eca864b30adfe22b048.png)

Consolidated Financial Statements Requirements And Examples

Chapter 3 An Introduction To Consolidated Financial Statements

Consolidated Statement Of Financial Position Workings Pdf

Consolidated Financial Statements Summary And Notes Huawei Annual

Chapter 6 Consolidated Financial Statements After Acquisition

:max_bytes(150000):strip_icc()/CSI-5bb2f4e2eb5948bab0415f1b76e47bbf.JPG)

Financial Statements List Of Types And How To Read Them

Ppt Concepts Of Consolidated Financial Statements Powerpoint

Consolidated Financial Statements With Aap Part 1 Module 5

Nice Transactions Consolidated Financial Statements Profit

Consolidated Statement Of Financial Position